Date: 24 April 2025

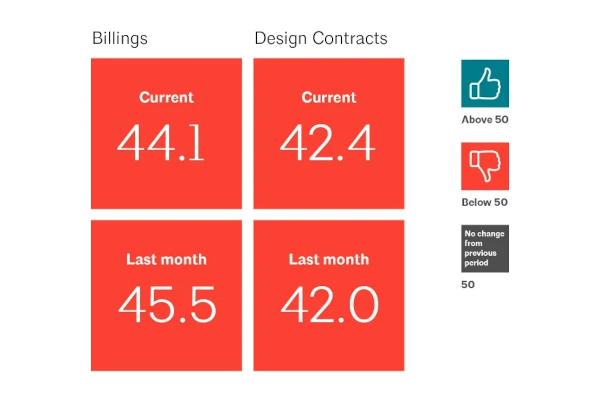

September 2022 marked the end of the post-pandemic billings surge for architects. Since then, billings have declined 27 of the last 30 months. For two consecutive months, inquiries into new projects have dropped, and newly signed design contracts have seen a decline for an unprecedented 13 months straight.

“Clients are increasingly cautious about starting projects due to uncertainty over future trends in interest rates and building materials costs, as well as the potential for an economic slowdown,” said Kermit Baker, PhD, Hon. AIA, AIA Chief Economist. “Unfortunately, this softness in firm billings is likely to continue as indicators of future work remain weak, however, the average project backlog at firms stands at a reasonably healthy 6.5 months, offering a bit of a buffer if future project work continues to remain soft.”

Key ABI highlights for March include:

- Regional averages: South (48.3); Midwest (45.5); West (43.0); Northeast (40.5)

- Sector index breakdown: institutional (46.2); mixed practice (firms that do not have at least half of their billings in any one other category) (46.1) commercial/industrial (45.1); multifamily residential (40.3)

- Project inquiries index: 47.7

- Design contracts index: 42.4

The regional and sector categories are calculated as three-month moving averages and may not always average out to the national score.

Visit AIA’s website for detailed information about this, and past billing index reports.

600450

600450

Add new comment